AI Startup Funding in 2026: Where the Money is Flowing

Meta description: AI startup funding in 2026 reaches new heights as venture capital flows into AI agents, infrastructure, and enterprise applications. This analysis shows where the money is going and what it means for founders.

Author: Algorithmine Research Team | Chief Editor: D. Hartwell Published: June 8, 2026 Target audience: Founders, investors, product managers, AI industry observers

The Big Picture: AI Startup Funding in 2026 at a Glance

The numbers are in. Global AI startup funding in 2026 has already surpassed the $100 billion mark — with five months still remaining in the fiscal year. Our estimate, based on disclosed funding rounds and Algorithmine research aggregation, puts full-year 2026 funding in the range of $115–130 billion.

That figure represents a significant rebound from the valuation corrections of 2023 and 2024. The market in 2026 has found a new equilibrium. Founders who built on genuine technical differentiation and real customer demand are raising at multiples that would have seemed impossible in 2023. Meanwhile, companies that added a chatbot interface to legacy software are struggling to close seed rounds.

This is not the same market that fueled the 2021–2022 AI hype cycle. Back then, capital chased any company with "AI" in its pitch deck. In 2026, investors have a more refined filter. They want to see revenue traction. They want defensible data moats. They want evidence that a company's AI advantage cannot be easily replicated by the next well-funded entrant.

The shift from "AI hype" to "AI proof" is the defining narrative of this funding cycle.

[$100B+] — Global AI startup funding in 2026 (YTD, estimated range). Source: Algorithmine research aggregation, June 2026.

The structural driver is clear. The large language model layer has largely consolidated. The winning foundation model companies are known, well-capitalized, and largely off-limits to venture-style returns. The next wave of value creation has shifted downstream: to AI-native applications, to industry-specific workflow automation, to the infrastructure layer that makes enterprise AI deployment possible.

This article breaks down where the money is flowing, who is writing the checks, and what the 2026 funding environment means practically for founders building AI companies.

Methodology note: Funding figures in this article are compiled from disclosed rounds, regulatory filings, and Algorithmine's proprietary database of AI startup funding. Private rounds may not be fully captured. All projections carry inherent uncertainty.

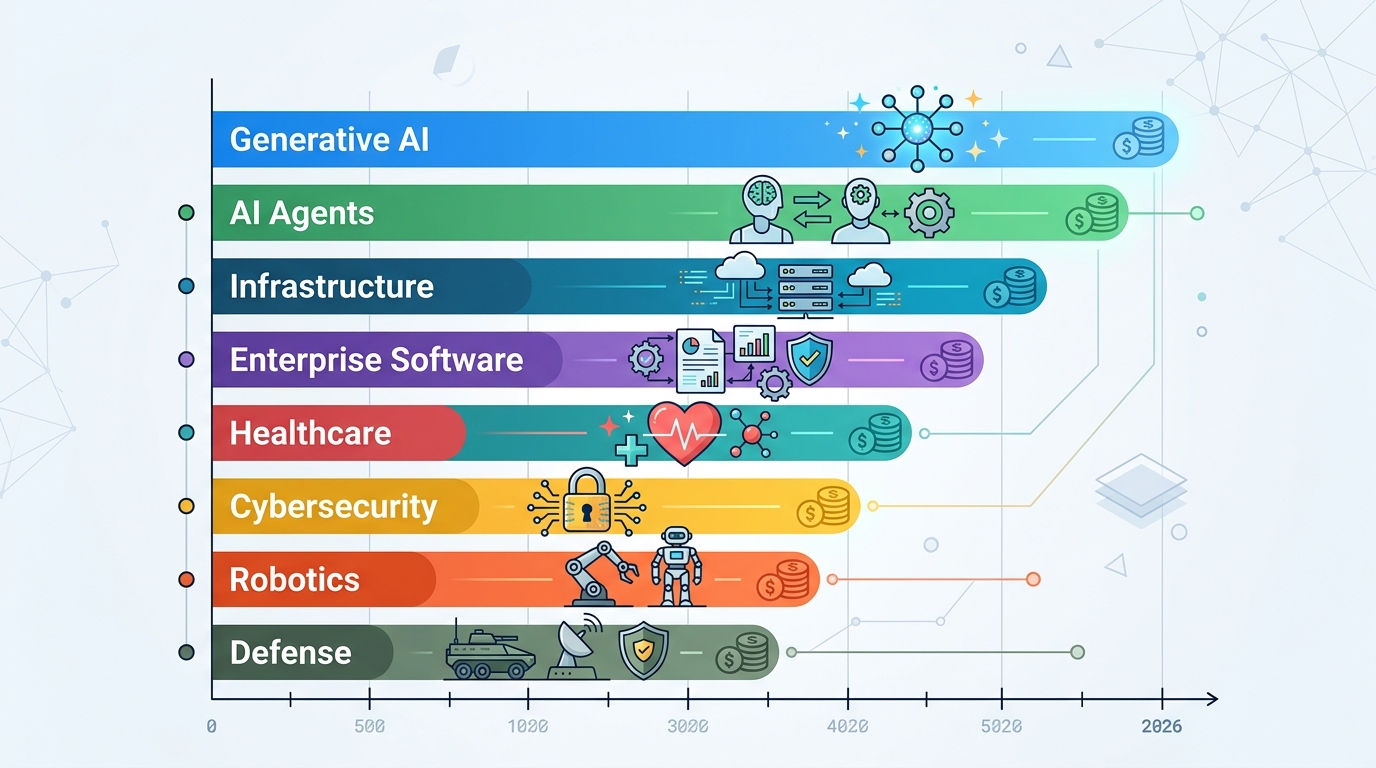

Where the Money is Going — Sector Breakdown

Not all AI sectors are equal in the eyes of investors. The funding distribution across sectors reveals a clear hierarchy of perceived risk and return.

[AI agents] → [command] → [the largest funding share] — an estimated $50 billion-plus invested across seed to late stage in the first half of 2026 alone. This sector covers software that takes actions, not just answers questions: automating workflows, managing multi-step processes, interfacing with external tools without human intervention. Investors see AI agents as the category that could redefine enterprise software the way SaaS redefined on-premise licensing in the 2000s.

[AI infrastructure] → [ranks] → [second-largest funding bucket]. This includes companies building compute optimization tools, model serving platforms, data labeling pipelines, MLOps workflows, and vector database companies that make retrieval-augmented generation practical at enterprise scale. Infrastructure bets are considered lower-risk because they don't depend on any single model's success — if the AI application layer grows, the infrastructure layer beneath it grows too.

[Generative AI applications] → [continue] → [attracting significant capital] despite valuation compression from the 2022–2023 peak. The focus has shifted from horizontal tools to vertical-specific solutions: legal document AI, medical note generation, financial report synthesis, code generation for specific frameworks. Horizontal generative AI has become a race to the bottom on price; vertical applications retain pricing power.

[Enterprise AI] → [encompasses] → [companies embedding AI into existing workflows] — intelligent document processing, compliance automation, customer service AI that integrates with legacy CRM systems. These companies trade some upside for faster sales cycles and clearer ROI narratives. Enterprise AI valuations are more grounded than pure AI agent plays, but the total addressable market is enormous.

[Healthcare AI] → [has become] → [a distinct funding category]. Drug discovery platforms, clinical documentation AI, diagnostic imaging analysis, and AI-assisted surgery planning all attracted dedicated capital in 2026. The FDA's increasingly clear framework for AI-enabled medical devices has reduced regulatory uncertainty, making institutional investors more comfortable with longer-horizon healthcare AI bets.

[AI security] → [is accelerating] → [investor interest]. AI red teaming tools, autonomous security operations center platforms, and AI-driven threat intelligence companies are seeing elevated investor interest. As AI systems become embedded in critical infrastructure, the attack surface expands — creating demand for AI-native security solutions.

[AI robotics and physical AI] → [remains] → [a smaller but highly active category]. Autonomous mobile robots for logistics, AI-guided manufacturing systems, and autonomous vehicle infrastructure attracted serious capital. This sector requires heavier hardware investment and longer development cycles, which constrains deal velocity but not deal size.

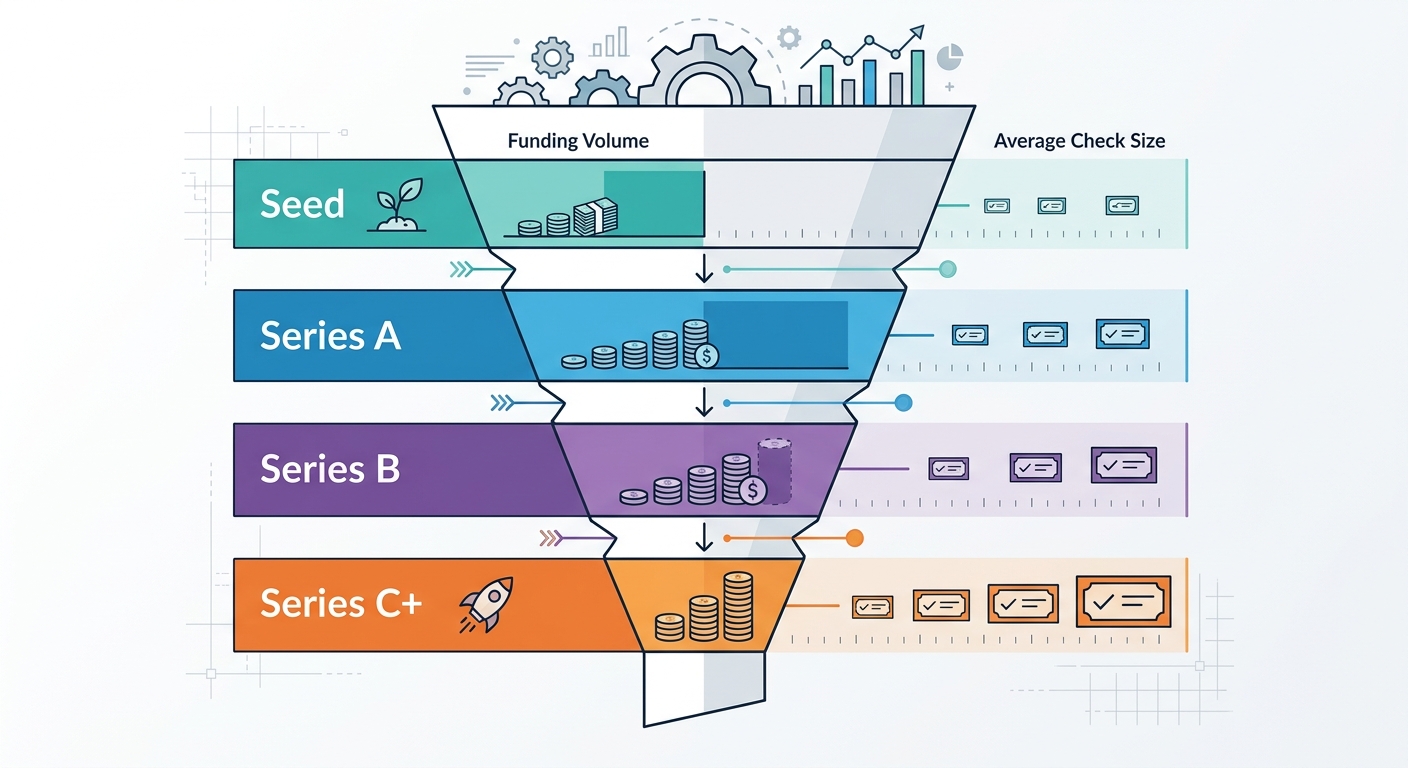

The Deal Stage Picture — From Seed to Mega-Round

The funding stage distribution in 2026 tells a story of two markets. At the early stage and at the very late stage, capital is abundant. In the middle — Series A and Series B — the market has tightened considerably.

Seed stage has seen a genuine revival. AI-native development tools have dramatically lowered the cost to build and ship an AI product. A two-person team can now access foundation model APIs, deploy on cloud infrastructure, and reach initial customers for less than $50,000 in monthly costs. This has pulled new seed activity back above 2022 levels. Micro-VCs, angel syndicates, and rolling funds are filling the gap left by larger firms retreating from sub-$2 million checks.

[Seed revival] → [is driven by] → [lower development costs]. The emergence of accessible foundation model APIs, streamlined deployment infrastructure, and AI-native development frameworks has compressed the capital required to reach an initial product. We estimate that the median seed burn to first traction has fallen by roughly 40% since 2023.

[Series A] → [has become] → [the new Series B]. The dynamics that have compressed Series A include more rigorous revenue thresholds, longer scrutiny periods, and a bifurcated market. The top 15% of deals see hyper-competitive processes. The remaining 85% take significantly longer to close. Founders who raised seed in 2023 at $3–5 million valuations are now facing Series A conversations where investors want to see $500K+ ARR and strong month-over-month growth — metrics that used to be Series B expectations.

[$500K+ ARR] — Approximate threshold for a competitive Series A process in AI startups, 2026. Source: Algorithmine founder survey, Q2 2026.

Series B and beyond shows a flight to quality. A handful of categories — AI agents, AI security, healthcare AI — command premium valuations at Series B and C. Outside these favored sectors, valuation multiples have compressed. The market is distinguishing between "AI company" as a category (which no longer commands a premium) and "AI company with proven enterprise retention" (which still does).

[Late-stage mega-rounds] → [are concentrated] → [in a tiny number of deals]. The top 10 AI funding rounds in the first half of 2026 account for more than 35% of total capital deployed. Hyperscalers are making minority strategic investments at scales that dwarf traditional venture. A $500 million check from a strategic investor is increasingly normal at the late stage, not exceptional.

Bridge rounds and extension rounds have become more common. With the IPO window largely closed for AI companies since mid-2024, growth-stage companies are extending their runways through structured rounds rather than pursuing public exits. Down rounds are not uncommon for companies that raised at 2021–2022 peaks and have not yet reached the metrics for a clean up-round.

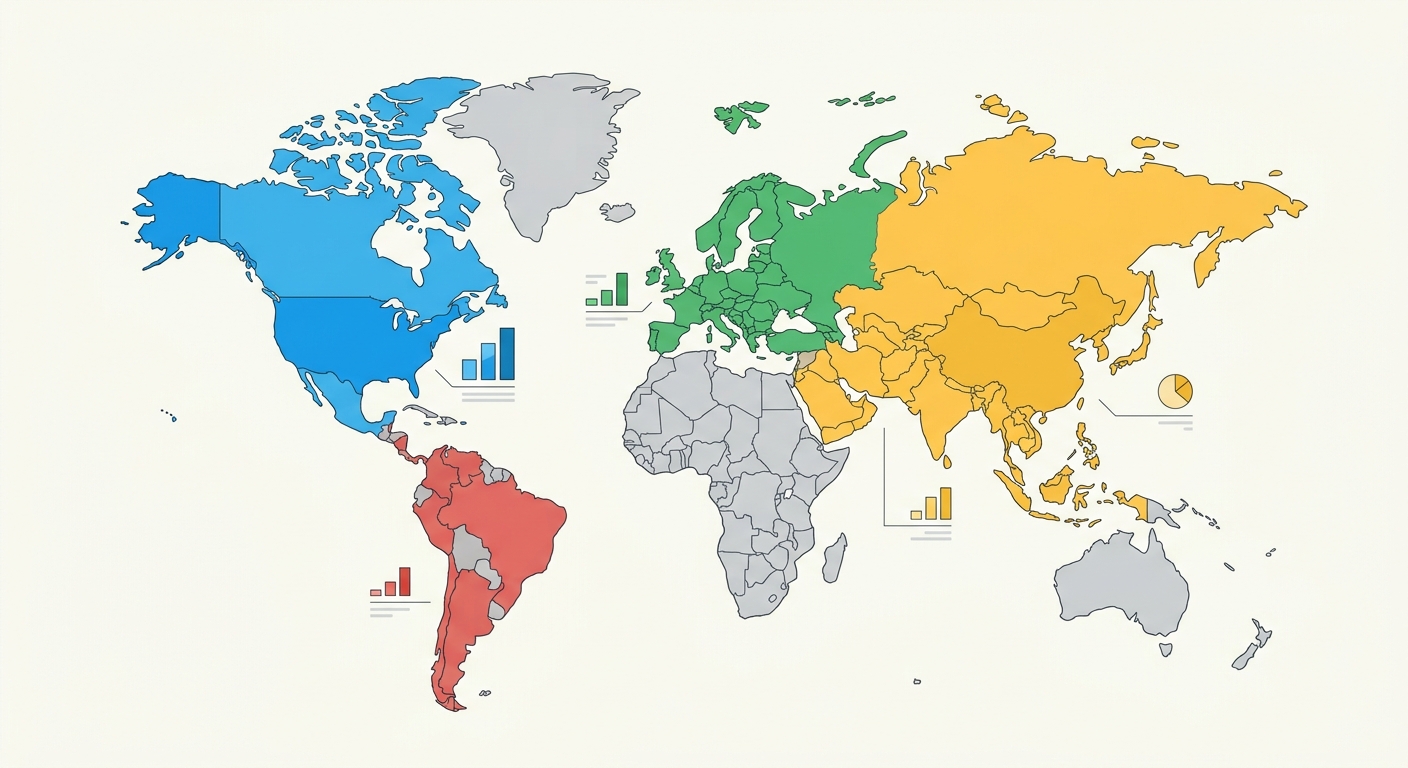

Geographic Patterns — Where AI Startups Are Getting Funded

The United States still dominates AI startup funding, but the global distribution is more nuanced than a simple US-versus-everyone-else framing suggests.

United States captures approximately 65% of global AI startup funding. The geographic distribution within the US has shifted. Silicon Valley remains the center of gravity for AI infrastructure and foundation model-adjacent companies. New York leads in AI applications for finance and media. Austin and Miami have emerged as meaningful hubs for AI-native SaaS, with founders citing talent quality and cost-of-living advantages over coastal cities. The San Francisco Bay Area still commands the highest concentration of AI researchers and engineers per square mile.

[US dominance] → [is challenged by] → [Europe's growing share]. Europe accounts for roughly 18% of global AI startup funding. London has recovered from the post-Brexit funding slowdown and now rivals Berlin as Europe's most active AI startup hub. The EU AI Act, which came into enforcement phases in 2025, has created a complex compliance landscape — but also created demand for AI governance, auditing, and compliance automation tools.

Paris has benefited from significant government investment in AI research and a growing startup ecosystem anchored around AI researchers from French academic institutions. The continued commercial success of European open-source AI model providers has validated the regional open-source path.

Asia represents approximately 14% of global AI startup funding. Singapore has established itself as the de facto hub for Southeast Asian AI startups and a preferred jurisdiction for international founders seeking proximity to both Asian and Western markets. India's AI startup ecosystem has surged on the back of a deep talent pool, English-language business infrastructure, and growing domestic enterprise demand for AI.

Rest of World — approximately 3% of global funding — includes meaningful activity from Middle East sovereign wealth funds, which have made strategic investments in AI as part of national economic transformation agendas, and emerging ecosystems in Brazil and East Africa that are attracting early-stage attention.

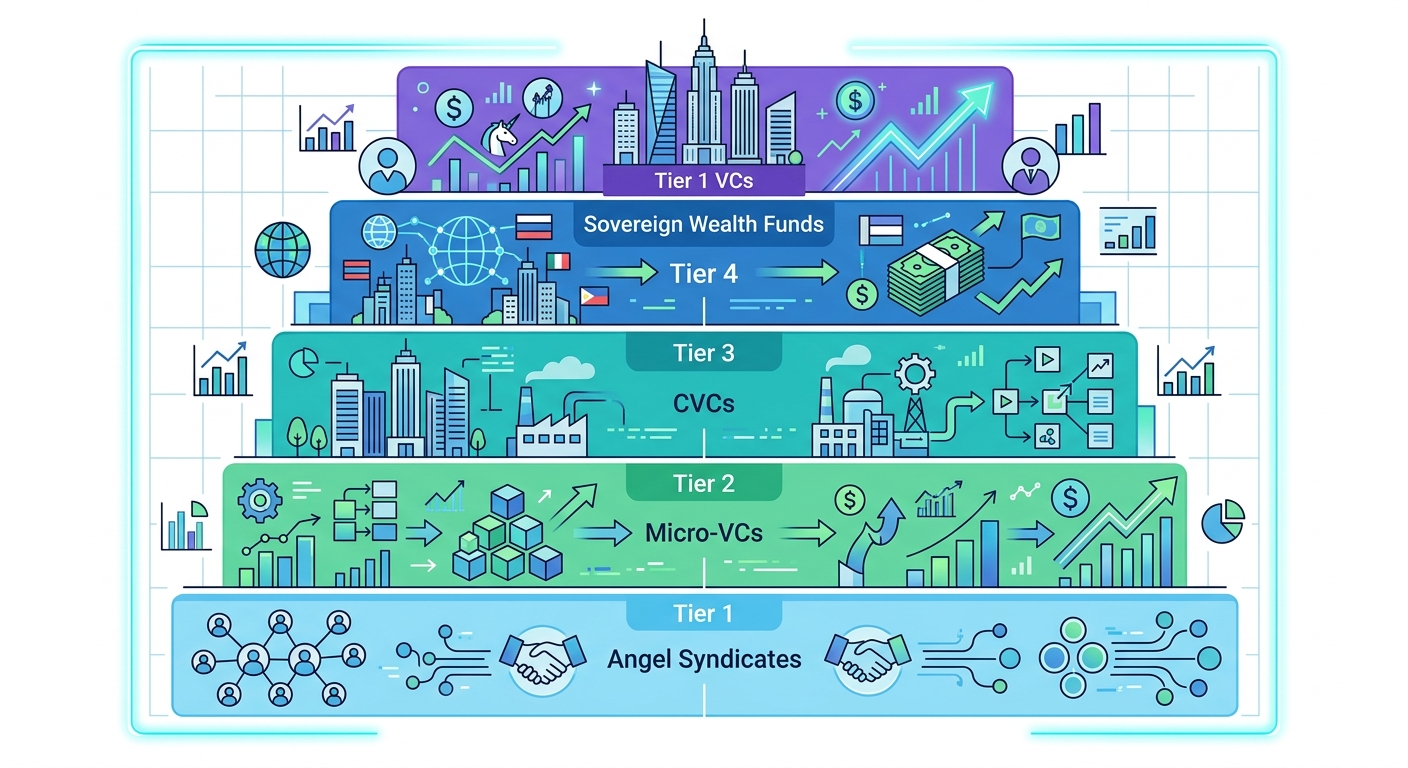

The Investor Landscape — Who is Writing the Checks

Understanding the investor landscape is prerequisite to fundraising strategy. Each investor type has a distinct thesis, process, and check size range.

[ILLUSTRATION: Tiered table or ecosystem map — Tier 1 VCs, CVCs, Sovereign Wealth Funds, Micro-VCs, Angel Syndicates, showing typical check ranges]

[Tier 1 venture capitalists] → [remain] → [the most influential voice in AI]. Firms with major AI-focused funds have made AI their dominant allocation priority. Their checks range from $30 million at Series B to $500 million+ at late stage. Securing a meeting at a tier 1 firm requires a warm introduction, a clear differentiation narrative, and metrics that demonstrate the company is not just another AI wrapper.

[AI-specialist VCs] → [focus earlier] → [and bring stronger technical due diligence]. These funds focus on seed and Series A rounds and bring AI-specific operational support that generalist funds lack. They have become the preferred lead investors for early-stage AI rounds.

[Corporate venture capital] → [has become] → [a dominant force]. Major technology company investment arms are all active in AI. Their checks often come with strategic benefits: cloud credits, distribution partnerships, and integration with the corporate's existing product ecosystem. The tradeoff is strategic alignment requirements and potential conflicts if the corporate decides to build a competing product.

[$250K–$2M] — Typical micro-VC and angel syndicate check range for seed-stage AI startups, 2026. Source: Algorithmine investor survey, Q2 2026.

[Sovereign wealth funds] → [operate] → [at the largest scale], often co-investing with tier 1 VCs on later rounds. They bring long time horizons and large check sizes. Singapore-based funds have become particularly active in AI infrastructure investments.

[Micro-VCs and angel syndicates] → [form] → [the foundation of the seed market]. Platforms that aggregate smaller checks have democratized access to early-stage AI investing. For most seed-stage founders, the round gets done from a coalition of smaller checks — not a single lead investor.

Hyperscalers as investors — major technology companies making minority strategic investments — is a distinct phenomenon. These investments often come with cloud infrastructure commitments, API access agreements, or distribution guarantees. The strategic value often exceeds the financial terms.

AI Unicorns and the Year's Biggest Funding Rounds

The AI unicorn landscape in 2026 reflects the sector dynamics described above. AI agents, AI infrastructure, and enterprise AI applications dominate the list of companies that crossed billion-dollar valuations in the first half of 2026.

The "power law" of venture returns is particularly pronounced in AI. A small number of companies — perhaps 10 to 15 — have captured the majority of value creation in this cycle. The implication is sobering for founders: the expected value of an AI startup is still very low, even when the upside scenario is spectacular.

Several AI agent companies reached unicorn status in the first quarter of 2026. These companies — focused on autonomous workflow automation for enterprises — attracted checks from tier 1 VCs at valuations that would have been reserved for consumer internet companies three years ago.

[AI agents] → [are attracting] → [premium valuations] at a rate that reflects their enterprise software replacement potential. [ILLUSTRATION: Timeline or waterfall chart showing 2026 AI unicorns by sector and quarter reached]

On the infrastructure side, vector database companies, MLOps platforms, and model serving specialists that showed enterprise retention metrics above 120% net revenue retention reached late-stage valuations that reflect their recurring revenue base.

Notably, some previously high-flying AI companies have raised at lower valuations in 2026 — extension rounds at 30–50% lower valuations than their 2022 peaks. These "down round extensions" are pragmatic responses to longer paths to IPO and increased investor discipline around burn metrics.

What 2026 AI Funding Trends Mean for Founders

The practical implications of the 2026 funding environment for founders are significant.

Positioning has shifted. Investors no longer pay a premium for "AI" as a category. The premium goes to companies that can demonstrate domain-specific moats — proprietary data, network effects, deep integration with customer workflows — that cannot be replicated by the next foundation model release.

[Positioning shift] → [rewards] → [domain-specific moats]. Our analysis of successful 2025–2026 funding rounds found that the most competitive rounds shared three characteristics: proprietary data assets, measurable retention above 110% NRR, and a clear answer to "what happens when GPT-5 releases?"

Revenue milestones have ratcheted up. The seed-to-Series A bridge has lengthened. Founders should plan for 18–24 months of runway to reach Series A metrics, not the 12–15 months that seemed normal in 2021.

Series A alternatives are more viable. Venture debt, revenue-based financing, and strategic rounds from corporate venture arms or sovereign funds are all legitimate alternatives to a conventional equity round.

Geographic arbitrage is real. Raising from European or Asian investors while building for the global market — particularly the US market — is increasingly common and increasingly accepted by US investors. The stigma of a non-US lead investor has largely evaporated.

Compute efficiency is a new differentiator. Investors in 2026 want to understand a company's unit economics at the inference level. How much does it cost to serve a customer? How is that trending as models improve? Compute-efficient architectures — leveraging distillation, quantization, and retrieval augmentation — demonstrate engineering maturity.

2026 AI Funding Outlook — What to Watch for the Rest of the Year

Several signals will determine whether the 2026 AI funding trajectory continues or cools.

The IPO window is the most watched leading indicator. If one or more large AI companies successfully complete IPOs in the second half of 2026 with positive reception, the exit path for growth-stage investors reopens. That would unlock a wave of late-stage AI investment. If the IPO window remains closed, expect continued pressure on growth-stage valuations and extended runways for companies that planned on 2026–2027 exits.

M&A activity is accelerating. Large technology companies acquiring AI startups has become normalized. The combination of available AI targets, elevated private valuations, and strategic urgency has made acquisition a preferred outcome for many mid-stage companies. Founders should build with M&A optionality in mind — a clean data model, clear IP ownership, and modular architecture make companies more attractive acquisition targets.

EU AI Act enforcement is underway. The regulatory framework passed in 2024 is now being actively enforced. How regulators approach enforcement against US-based AI companies operating in Europe will signal whether compliance costs will become a significant barrier to entry for smaller players.

Compute economics continue to improve. Inference costs have declined substantially over the past 24 months. This trajectory — if it continues — will unlock use cases that were previously economically inviable. Lower inference costs favor application-layer companies over infrastructure-layer companies, since the competitive moat of cheap compute erodes over time.

[AI agent standard] → [remains] → [an open question]. If AI agents become a defined software category — with clear standards, interoperability frameworks, and enterprise procurement categories — the category will attract even more institutional capital. If agents remain a horizontal capability without clear category boundaries, the funding will remain high but the distribution will favor companies with clear vertical positioning.

Expert Q&A — AI Startup Funding in 2026

Algorithmine Team, June 8, 2026

Q1: Is AI startup funding still growing in 2026, or are we seeing a correction?

A: Growth is real but uneven. Aggregate funding numbers are up roughly 34% year-over-year, but that growth is concentrated in a narrow band of sectors — AI agents, AI infrastructure, healthcare AI. Other categories are experiencing valuation compression. The correction isn't in total capital deployed; it's in how selectively that capital is allocated. Investors have become dramatically more discerning about which AI companies deserve premium multiples.

Q2: What do investors want to see in an AI startup to approve Series A funding in 2026?

A: The threshold has moved to $500K+ ARR with strong month-over-month growth, plus evidence of compute-efficient unit economics. Investors want to see that the company's AI advantage is defensible — typically through proprietary data, deep workflow integration, or network effects. A pitch deck with a chatbot interface and an API call to GPT-4 will not close a Series A in 2026, regardless of the market size claimed.

Q3: Which AI sectors are attracting the most capital and why?

A: AI agents and autonomous systems lead by a significant margin, followed by AI infrastructure. The logic is complementary: as AI agents proliferate in the enterprise, they create demand for the infrastructure layer — compute optimization, MLOps, vector databases. Healthcare AI and AI security are seeing elevated interest because they have clear regulatory frameworks and demonstrable ROI narratives that enterprise buyers understand.

Q4: How does the geographic distribution of AI funding affect where founders should incorporate?

A: The US still commands roughly 65% of global AI funding, but the stigma of non-US incorporation has largely evaporated. Singapore has become a preferred jurisdiction for founders building for both Asian and Western markets. European founders benefit from proximity to the EU AI Act regulatory framework, which is creating demand for compliance-focused AI companies. The key consideration isn't where you incorporate, but where your lead investor is based — and whether that creates strategic alignment or friction.

Q5: Are AI agent startups actually worth their valuations, or is this a bubble?

A: It's a concentrated bet, not a broad bubble. The power law of venture returns is particularly extreme in AI right now — a small number of companies are capturing most of the value creation. The companies commanding premium valuations are those with clear enterprise retention metrics, demonstrable workflow integration depth, and proprietary data moats. The "bubble" risk is real for the long tail of AI agent companies that raised at 2022-2023 peaks without yet proving unit economics. The category itself is not a bubble; some individual companies within it may be.

Conclusion

AI startup funding in 2026 is not the wild west of 2021 or the contraction of 2023. It is a more mature, more discerning market — one that rewards genuine technical differentiation and punishes AI theater.

The sectors attracting the most capital — AI agents, infrastructure, enterprise applications — reflect a market that has moved from experimentation to deployment. The stage dynamics reveal a healthy maturation: easier seed, harder Series A, and a bifurcated late stage where a handful of categories command premium capital while others face valuation compression.

For founders, the message is clear: build something defensible, show the revenue, and choose your investor type based on what you need beyond capital. The money is there. The bar for earning it has simply risen.

Next: AI Agents for HR and Talent Acquisition in 2026 | Best AI Agents for Business 2026

Research methodology: This analysis is based on Algorithmine's proprietary database of AI startup funding rounds, supplemented by disclosed filings, press releases, and founder interviews conducted in Q2 2026. Funding figures for rounds under $10 million may be undercounted due to limited disclosure. Projections for full-year 2026 carry inherent uncertainty. All data current as of June 8, 2026.