AI Startup Funding Report Q2 2026: Where Investors Are Placing Their Bets

Q2 2026 AI startup funding is tracking toward $95B–$110B, making it the largest AI funding quarter in history. Here is where investors are placing their bets.

The AI funding boom is not slowing down — it is accelerating. In Q2 2026, global AI startups are tracking toward $95 billion to $110 billion in disclosed funding, making it the largest AI funding quarter in history. This surge builds on Q1 2026's approximately $87 billion and shows no signs of plateauing.

What makes this moment distinct from previous AI hype cycles is the structural shift in how capital is deployed. Venture capital is concentrating in AI at an unprecedented rate — roughly 80% of all global VC in Q1 2026 flowed into AI companies. The numbers are not just large; they are reshaping the entire venture landscape.

This report breaks down where the money is actually going, which investors are leading the largest deals, which sectors are attracting the most capital, and what the risks are for the second half of 2026.

AI Funding in Q2 2026 — By the Numbers

Q2 2026 is on track to shatter every previous AI funding record. The first half of 2026 saw record-breaking venture capital investments driven by substantial rounds for companies like OpenAI and Anthropic, according to the NVCA PitchBook data.

The scale is staggering. Global AI startup funding for Q2 is tracking between $95 billion and $110 billion. That is more than the entire annual VC deployment of most years prior to 2022.

Why the sudden acceleration? Several factors converge. Foundation model companies are requiring increasingly large capital bases to train and serve models. Infrastructure buildout is capital-intensive. And investor conviction in AI's transformative potential has reached a level that is drawing capital away from every other sector.

Roughly 80% of all global venture capital deployed in Q1 2026 went into AI companies, leaving other sectors competing for the remaining 20% of available funding.

The skew is not a temporary aberration. Multiple investors and fund managers have indicated that they are structurally overweight AI for the foreseeable future. That creates a self-reinforcing dynamic: AI companies get the best terms, the best investors, and the best talent, while non-AI startups face a narrower funding environment.

The Mega-Round Dominance — Where the Big Money Flows

Capital concentration in AI is extreme. The top 10 AI funding rounds in Q2 2026 account for over 60% of total AI funding for the quarter. A small number of companies are capturing an outsized share of available capital.

The late-stage bias is equally striking. Approximately 82% of all venture capital deployed in Q1 2026 went to late-stage rounds exceeding $100 million. For early-stage investors looking to deploy into new companies, the landscape has narrowed considerably.

Who is writing the largest checks? Sovereign wealth funds have become the marginal buyers in the biggest AI rounds. MGX, HUMAIN, GIC, Temasek, and Mubadala are increasingly leading or co-leading rounds exceeding $1 billion. These are patient, strategic investors with long time horizons and national-level resources.

Among traditional venture firms, SoftBank, Andreessen Horowitz, Sequoia, Thrive Capital, and Lightspeed Venture Partners are the most active across seed, Series A, and Series B deals. These firms have collectively signaled that AI represents their highest conviction allocation for the decade.

The implication for founders is clear: if you are building an AI company and targeting late-stage funding, sovereign wealth capital is now a primary target. The relationships, the terms, and the strategic value these investors bring have made them the preferred partner for the largest rounds.

The New Revenue Bar — What Investors Are Demanding from AI Startups

The old narrative — that investors fund AI companies on potential alone — is outdated. In 2026, revenue expectations have hardened across every funding stage.

Series A rounds in AI now typically require $1 million to $3 million in Annual Recurring Revenue. Series B investors are looking for over $10 million in ARR before committing. These thresholds have risen sharply from two years ago, when much lower revenue numbers could support large rounds.

Series A rounds in AI now require $1M–$3M ARR, while Series B expects $10M+ ARR — a significant jump from two years prior, reflecting investor emphasis on commercial traction over technical potential.

This creates a bifurcated market. Companies that can show real revenue get access to the cheapest and largest capital. Companies still in the research or early-product phase face a much narrower set of investors willing to take a chance.

For founders, the implication is to pursue revenue earlier than in previous cycles. The days of raising a large Series A on the basis of impressive demos are fading. Investors want to see that customers are paying, that the product is sticky, and that the revenue is recurring.

The AI Sectors Getting Funded Right Now

Beneath the headline numbers, specific sectors are commanding disproportionate investor attention. Here is where capital is flowing.

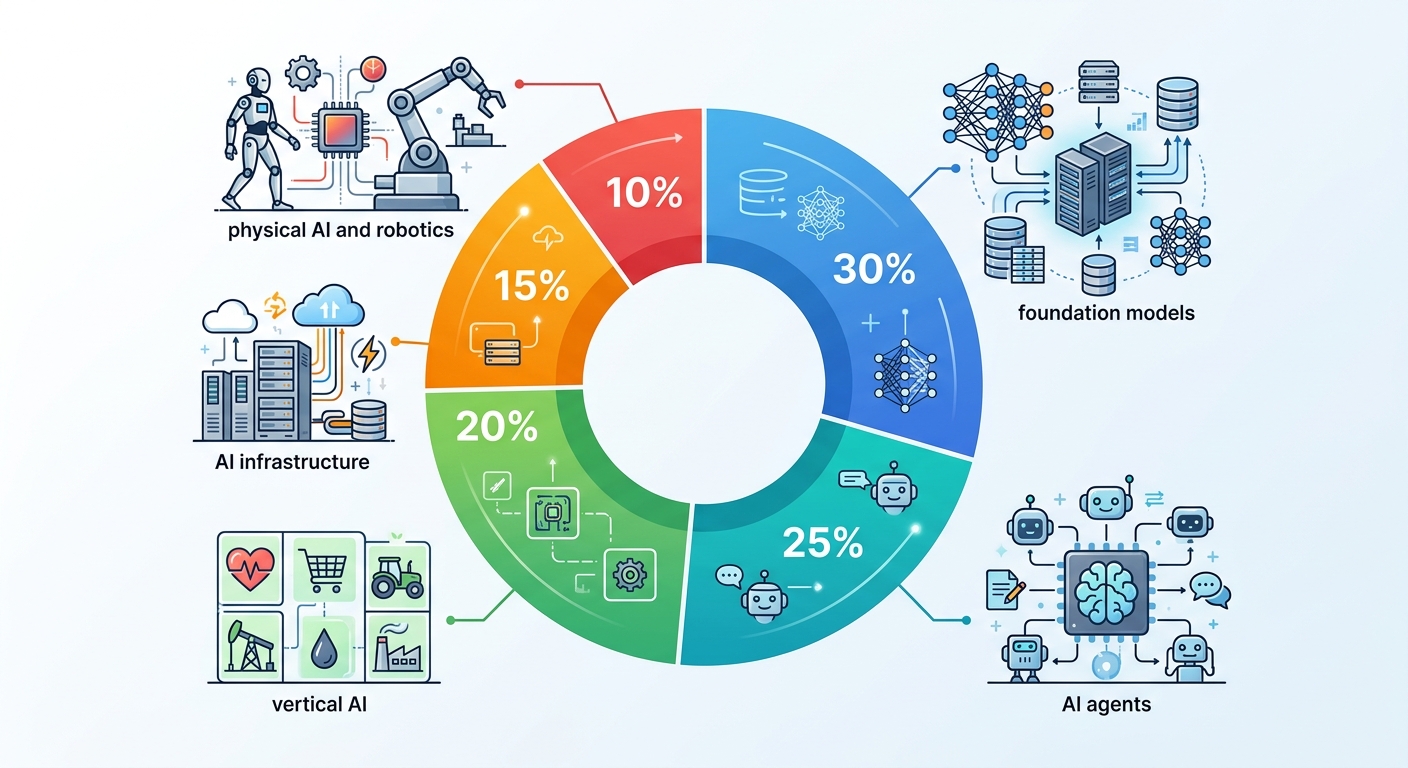

Foundation Model Labs

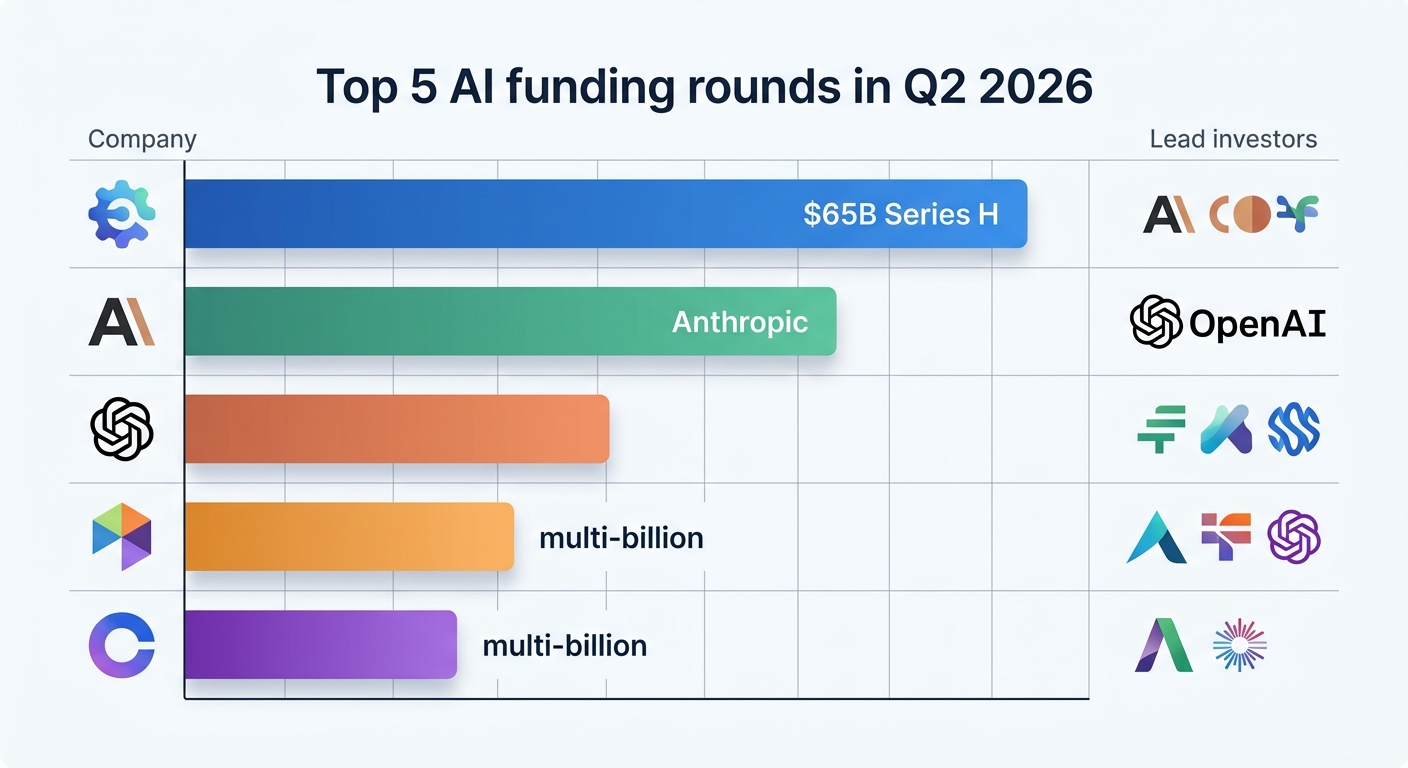

The largest funding rounds still go to foundation model companies. OpenAI, Anthropic, xAI, and Mistral AI continue to secure multi-billion-dollar rounds to train and serve increasingly capable models.

Anthropic is a standout case. The company surpassed OpenAI in private valuation, reaching $965 billion after a $65 billion Series H round in late May 2026. That single round is larger than most industries' annual VC totals.

AI Agents — The Breakout Category

AI agents have emerged as the most significant new funding category in 2026. These are systems that autonomously execute multi-step workflows — automating customer service, business processes, software development, and decision support.

Sierra, Decagon, and Cognition are among the startups attracting substantial investment in this space. The thesis is straightforward: after the foundation model layer matures, the value shifts to applications that use models to take actions in the world. Agents are that application layer.

Vertical AI — Deep Industry Specialization

AI solutions tailored to specific industries are considered one of the strongest categories for new founders. The advantage is clear: domain-specific training data creates defensible moats that general-purpose models cannot easily replicate.

In legal AI, Harvey and EvenUp are well-funded and growing. In healthcare AI, Abridge, OpenEvidence, and Hippocratic AI are deploying AI for clinical documentation and decision support. Both sectors have dense, structured data and clear ROI cases for AI automation.

AI Infrastructure — The Enabling Layer

Companies building the plumbing for the AI boom continue to raise significant capital. Perplexity is redefining AI-native search. Glean is building enterprise knowledge management. Cohere is providing enterprise AI infrastructure that competes with Big Tech's offerings.

Infrastructure companies benefit from the AI buildout regardless of which foundation model or application wins. They are the picks-and-shovels of the AI gold rush.

Physical AI and Humanoid Robotics

The most speculative — and most discussed — category is physical AI, where machine learning meets the physical world. Project Prometheus and companies deploying humanoid robots at Amazon, BMW, and Mercedes are drawing significant investor interest.

The capital requirements are enormous. Hardware is expensive, timelines are long, and the technical challenges are severe. But the potential upside and the strategic importance of physical AI capability has drawn substantial funding.

Big Tech's $600 Billion AI Bet

Major technology companies are projected to spend nearly $600 billion on AI in 2026. That number dwarfs the entire startup funding ecosystem and deserves separate analysis.

Where is this capital going? Primarily to infrastructure: GPU clusters, data centers, and power procurement. This is not venture capital in the traditional sense — it is an industrial-scale buildout of computing capacity.

A significant portion of Big Tech AI spending is going to strategic minority investments rather than acquisitions. Rather than buying startups outright, large tech companies are taking stakes in AI companies and AI infrastructure providers. This preserves startup independence while giving Big Tech optionality on emerging technology.

For AI startups, Big Tech's infrastructure investment is largely beneficial. The cloud providers are building the compute layer that startups depend on. As GPU availability expands and costs decline, the unit economics of AI applications improve across the board.

The Exit Landscape — IPO Supercycle Begins

The venture capital-backed exit market for AI has developed a characteristic barbell shape. On one end, a small number of strategically significant deals with well-capitalized acquirers at high valuations. On the other end, a large number of undisclosed-value transactions that offer limited returns.

2026 has seen the beginning of an IPO supercycle. Cerebras launched its IPO in May 2026 — the first major AI-focused public offering of this cycle. OpenAI and Anthropic have both signaled plans to go public, with Anthropic's $965 billion private valuation already exceeding most public technology companies.

Anthropic's valuation now surpasses OpenAI's after its $65 billion Series H in May 2026, reflecting investor conviction in its enterprise-focused AI strategy and the Claude model's commercial traction.

For startup founders, the IPO momentum matters because it creates a viable exit path beyond acquisition. If the public markets continue to value AI companies at premium multiples, the path to a 2027 or 2028 IPO becomes real for a new generation of AI startups.

Risks and Headwinds — What Could Derail the AI Funding Boom

No market analysis is complete without examining risks. Several factors could disrupt the current AI funding environment.

Regulators have initiated investigations into talent acquisition practices at major technology companies, including Microsoft and Google. These probes could slow down the talent market consolidation that has been driving AI capability concentration.

Geopolitical risk is increasing. China's order to unwind Meta's $2 billion acquisition of Manus in April 2026 illustrates how cross-border AI deals are exposed to national security review. Investors are beginning to price this risk into international AI transactions.

The ROI accountability pressure is perhaps the most significant near-term risk. Organizations are increasingly demanding measurable returns on their AI investments. CFOs are scrutinizing AI spending with greater rigor. If the productivity gains from AI fail to materialize at scale, the next round of budget allocations may tighten.

The most likely correction scenario is not a crash but a recalibration. Capital will remain abundant for AI companies that can demonstrate commercial traction and clear ROI, while the "potential alone" trade becomes much harder to fund.

For investors, the second half of 2026 will be a test of conviction. The AI thesis has been validated at the macro level. The question is whether individual portfolio companies can convert that macro momentum into measurable commercial success.